Line 260 - Adjustment of investment expenses

Line 260 - Adjustment of investment expenses

Line 260 - Adjustment of investment expenses

The investment expenses you deduct cannot exceed your investment income. If you are claiming one or more of the following deductions, complete Schedule N to calculate the amount to enter on line 260 of your return:

-

a deduction for a loss from a partnership of which you were a specified member (included on line 29 of Schedule L or line 136 of your return);

-

a deduction for carrying charges and interest expenses (line 231 of your return);

-

a deduction for exploration and development expenses (line 241 of your return);

-

a deduction for other expenses that you incurred to earn property income, including the following deductions:

-

a deduction for the repayment of interest received,

-

a deduction for certain films (line 250 of your return),

-

a deduction for foreign income tax on income from property other than rental property (line 250 of your return),

-

a deduction for life insurance premiums relating to property income that is not rental income,

-

a deduction for the repayment of an advance on a life insurance policy (line 250 of your return).

-

In calculating the adjustment of investment expenses, do not take into account any amount for a bad debt deducted in the calculation of property income.

Exploration and development expenses

(line 14 of Schedule N)

On line 14 of Schedule N, enter the result of the following calculation:

-

Add up the following amounts:

-

the amount claimed for renewable and conservation expenses incurred in Québec (box 60-2 of the RL-15 slip or box A-1 of the RL-11 slip);

-

the amount claimed for Québec development expenses (box 61-1 of the RL-15 slip or box B-1 of the RL-11 slip); and

-

the amount claimed for Québec exploration expenses that do not give entitlement to an additional deduction (box 60-1 of the RL-15 slip or box A-2 of the RL-11 slip).

-

-

Subtract the total from the amount on line 241 of your return.

-

Multiply the result by 50%.

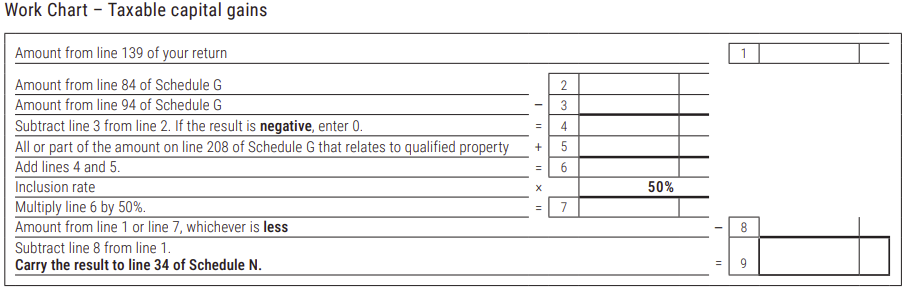

Taxable capital gains

(line 34 of Schedule N)

On line 34 of Schedule N, enter the amount from line 139 of your return if it does not include a capital gain that entitles you to the capital gains deduction (line 292), which would be calculated in form TP-726.7-V, Capital Gains Deduction on Qualified Property.

If you realized capital gains that entitle you to the capital gains deduction on line 292, complete the work chart below.

Carry-over of the adjustment of investment expenses

If you are entering an amount on line 260 or 276 to adjust your investment expenses, you can use all or part of that amount to reduce your net investment income for the previous three years or for future years. To calculate your net investment income for a year, use Schedule N. Complete lines 20 through 36 to determine your investment income, and then subtract your investment expenses (lines 10 through 16, 50 and 52) from the amount on line 36. If you want to reduce your net investment income for previous years, complete form TP-1012.B-V, Carry-Back of a Deduction or Tax Credit, and file it separately from your return.