69 Business investment loss

69 Business investment loss

A business investment loss is a capital loss that the trust sustained on the disposition of a share of the capital stock of a small business corporation (that is, a CCPC all or substantially all of the FMV of whose assets is attributable to assets used in an eligible business that the corporation carries on primarily in Canada). A business investment loss may also be sustained on the disposition of a debt obligation owed by a small business corporation or owed by a CCPC:

-

that became bankrupt while carrying on a small business; or

-

that, pursuant to section 6 of the Winding-up and Restructuring Act, was insolvent within the meaning of this Act at the time a winding-up order was rendered but had been carrying on a small business at that time.

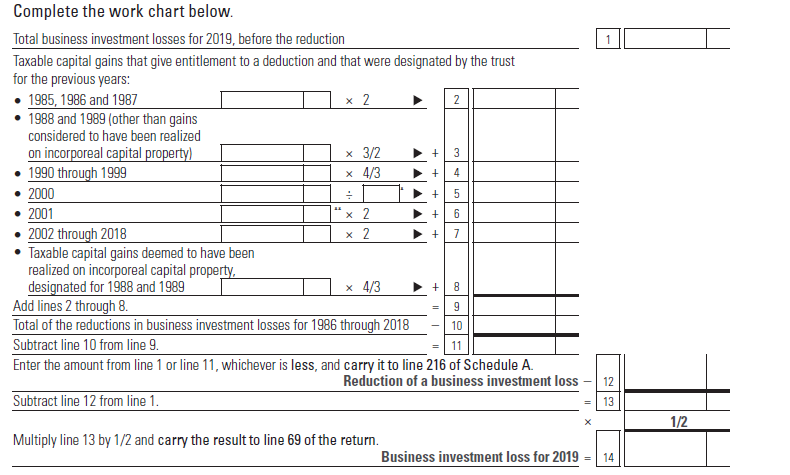

* Enter the inclusion rate applicable to the trust for 2000 and divide.

** If the inclusion rate applicable to the trust is not 1/2, do not multiply this amount by 2. Instead, divide it by the applicable rate and enter the result on line 6.

A loss sustained in one of the following situations is considered to be a business investment loss:

-

The corporation that operates the business is a small business corporation at the time of the disposition.

-

The trust disposed of the share or debt obligation to a person dealing with the trust at arm's length.

-

The trust has made an election whereby it is deemed to have disposed of the share or debt obligation at the end of the year, for nil proceeds, and to have reacquired the share or debt obligation immediately thereafter at nil cost. Consequently, the amount of the loss is equal to the amount of the debt obligation or to the ACB of the share immediately prior to the disposition. The trust must enclose with its return a letter advising us that it is electing to have the provisions of section 299 of the Taxation Act apply to the share or debt obligation.

For more information, see Capital Gains and Losses (IN-120-V).

Business investment losses must be reduced by the amounts the trust allocated to the beneficiaries in a previous year and that the trust designated as taxable capital gains that give entitlement to a deduction. The amount of the reduction (line 12 of the work chart) is considered a capital loss and must be carried to line 216 of Schedule A.

The allowable business investment loss is determined on line 14 of the work chart, and can be deducted on line 69 of the return. If the amount of the allowable business investment loss exceeds the trust's income for the year, the excess amount is included in the calculation of the non-capital loss (see the instructions for lines 90 and 99).

|

NOTE The portion of a non-capital loss that is attributable to the allowable business investment loss can be carried to the three previous taxation years and the ten subsequent taxation years. Any amount that cannot be deducted as a non-capital loss for these years becomes a net capital loss. |

231, 232.1, 264.5, 299, 300

|

|

|