Line 123 - Tax credit for donations and gifts

Line 123 - Tax credit for donations and gifts

Line 123 - Tax credit for donations and gifts

Only consider eligible gifts and donations for which the trust has an official receipt from the donee for the purposes of calculating the tax credit for donations and gifts.

Gifts made under a will

A gift made by will or by designation is deemed to be made by the succession at the time the property (or property substituted for the property) is transferred to the donee.

If a GRE (or a succession that ceased to be a GRE solely because it existed for more than 36 months after the death) makes a gift (or is deemed to have made a gift) within 60 months following the death, the gift can be:

-

allocated to the deceased and included in their income tax return for the year of the death or the previous year;

-

included in the income tax return of the GRE for the year of the transfer or a previous year; or

-

included in the income tax return of a succession that was a GRE in the year of the transfer.

These rules apply if the deceased left the proceeds of a registered retirement savings plan (RRSP), a registered retirement income fund (RRIF) or a tax-free savings account (TFSA) to a qualified donee under a will. They also apply if the deceased designated a qualified donee as the beneficiary of the proceeds of an insurance policy in Canada.

The tax credit for donations and gifts can be claimed in the deceased's income tax return for the year of death or in an income tax return for a preceding year, even if the gifted property has not yet been transferred to the qualified donee. In this situation, you will have to provide a copy of all of the following documents:

-

the will;

-

a letter from the succession to the charitable organization informing it of the gift and providing details and an estimated value of the property being gifted;

-

a letter from the charitable organization acknowledging the gift and stating that it accepts it;

-

a statement or letter from the succession's legal representative stating all of the following:

-

the succession is a GRE of the deceased individual and will be designating itself as such,

-

the succession intends to make the gift within 60 months after the date of death,

-

the succession intends to claim the tax credit for donations and gifts in the deceased individual's income tax return and not in the succession's return,

-

for future non-cash gifts, the value of the gift can be reasonably determined and supported.

-

Sections 232 and 752.0.10.10.0.1

Cultural patronage or large cultural donation made upon a death

It is presumed that a gift made by will or by designation is deemed to be made by the succession of the deceased individual at the time the property is transferred to a qualified donee. This presumption also applies to a donation that gives entitlement to the additional tax credit for a large cultural donation. However, a succession cannot claim a tax credit for such donations.

A large cultural donation made by a GRE within 36 months following the death can be used to reduce the income tax payable by the deceased individual for the year of the death or the previous year.

Note that the tax credit for cultural patronage was eliminated on March 26, 2025. However, a succession that registered a pledge with the Minister of Culture and Communications on or before March 25, 2025, can claim the tax credit under the current terms and conditions. Furthermore, registered pledges remain subject to the provisions for failure to honour a pledge.

The elimination of the tax credit for cultural patronage does not affect the carry-forward and carry-back periods of the individual or the individual's succession, in respect of a patronage gift made before March 26, 2025.

If a gift is made in more than one payment, the value of the gift must be reported on line 406 of Schedule C and deducted on line 81 of the return, like any other allocation of income to beneficiaries. The amount on line 406 must also be reported on an RL-16 slip.

If the will allows a gift to be made at the trustee's discretion, the trustee can either proceed as explained in the previous paragraph (as though the gift is being made in more than one payment), or claim a tax credit on line 123.

In all cases, you must specify in the return whether the payment was made according to instructions in the will or at the discretion of the trustee.

Gifts made by an inter vivos trust

If the trust is an inter vivos trust and the donee is a beneficiary of the income under the trust deed, the value of the gift must be reported on line 406 of Schedule C and deducted on line 81 of the return as an allocation of income to the beneficiaries of the trust. In all other cases, a tax credit can be claimed on line 123.

The total amount of the tax credit for donations and gifts that a trust other than a GRE or a QDT can claim for a taxation year is equal to:

-

20% of either $200 or the trust's total eligible donations and gifts for the year (whichever is less); and

-

25.75% of the amount by which the trust's total eligible donations and gifts for the year exceeds $200.

The total amount of the tax credit for donations and gifts that a GRE or a QDT can claim for a taxation year is equal to the total of the following amounts:

-

20% of either $200 or the trust's total eligible donations and gifts for the year (whichever is less);

-

25.75% of the lesser of the following amounts:

-

the amount by which the trust's total eligible donations and gifts for the year exceeds $200,

-

the amount by which the trust's total income for the year (line 99 of the return) exceeds the threshold of the fourth income tax bracket for the year;

-

-

24% of the amount by which the trust's total eligible donations and gifts for the year exceeds the aggregate of $200 and the amount of donations and gifts to which the rate of 25.75% applies.

Section 752.0.10.6

Gifts made by a religious organization

Under federal legislation, a trust that is a religious organization can elect to waive its right to the tax credit in favour of the adult members of the organization, provided it designates its charitable donations and other gifts. Consequently, designated amounts will be considered gifts made by the members, not by the trust. For the purposes of Québec legislation, no such election can be made unless it is made under federal legislation, in which case it is automatically deemed to be made. Therefore, if the trust makes this election with the Canada Revenue Agency (CRA), you must send us proof that the election was made and written notification no later than the filing deadline for the trust income tax return or 30 days after the election was made (whichever is later).

Refer to section 3.2.16 of the Guide to Filing the RL-16 Slip: Trust Income (RL-16.G-V).

Section 851.33

Food donations made by a trust that carries on a farming business

The eligible amount for food donations can be increased by 50% if the donations are made by a trust that carries on a business that is considered to be a recognized farm producer. The donations must also have been made to a registered charity that was a member of the Food Banks of Quebec network (either a Moisson member or associate member).

Recognized farm producer

The term "recognized farm producer" means an individual or a corporation that carries on a farming business registered as an agricultural operation with the Ministère de l'Agriculture, des Pêcheries et de l'Alimentation, in accordance with the regulation adopted under section 36.15 of the Act respecting the Ministère de l'Agriculture, des Pêcheries et de l'Alimentation. The term also means a member of a partnership carrying on such a business at the end of the partnership's fiscal period.

Eligible agricultural product

The term "eligible agricultural product" means any product grown, raised or harvested by a registered agricultural operation, provided the product can be legally sold, distributed or offered for sale-at a place other than where it was produced-as a food or beverage intended for human consumption. Examples of eligible agricultural products are meat and meat by-products, eggs and dairy products, fish, fruit, vegetables, grain, legumes, herbs, honey, maple syrup, mushrooms and nuts.

Sections 716.0.1.4 and 752.0.10.15.6

Food donations made by a trust that carries on a food processing business

The eligible amount for food donations can be increased by 50% if the donations are made by a trust that carries on a food processing business. The donations must also have been made to a registered charity that was a member of the Food Banks of Quebec network (either a Moisson member or associate member).

Eligible food donations include milk, oil, flour, sugar, frozen vegetables, pasta, prepared meals, baby food and infant formula.

Sections 752.0.10.1 and 752.0.10.15.6

Charitable donations

Charitable donations are donations made to qualified donees that are not gifts of cultural property, ecological gifts or gifts of musical instruments (for instructions see Other gifts).

The term "qualified donee" includes:

-

a registered charity;

-

a registered Canadian or Québec amateur athletic association;

-

a corporation constituted exclusively for the purpose of providing low-cost housing accommodation for senior citizens;

-

a registered cultural or communications organization;

-

a registered Canadian municipality;

-

the United Nations or one of its agencies;

-

a registered foreign university;

-

the Government of Canada or a provincial government;

-

the Organisation internationale de la Francophonie or one of its subsidiaries;

-

a registered museum;

-

a registered municipality or public body performing a function of government in Canada;

-

a recognized political education organization; and

-

a registered journalism organization.

Limit regarding the charitable donation of a work of art

If, during the taxation year, the trust donated a work of art, the value of the donation can be deducted as income allocated to the beneficiaries of the trust (line 81) or may qualify for a tax credit for donations and gifts (line 123), provided the donee sells the work of art on or before December 31 of the fifth year following the calendar year in which the donation was made. If the trust cannot take the donation into account at the time the return is filed because a receipt has not yet been issued, it can request an adjustment from us after obtaining the receipt using form TP-646.R-V, Request for an Adjustment to a Trust Income Tax Return.

The five-year time limit does not apply if the work of art was donated:

-

to a registered museum, if the gift is cultural property;

-

to a registered Canadian municipality, the Government of Canada or a provincial government or an organization that acquired the work as part of its primary mission;

-

to a charity that is a recognized institution or establishment for the purpose of the 50% increase in the eligible amount of the donation, if the work of art is a public work of art (refer to the information below).

Increase in the eligible amount of a donation of a work of art

The eligible amount of a donation of a work of art to a museum in Québec or a museum that has the status of a recognized or accredited museum from the Minister of Culture and Communications can be increased by 25%.

However, if a trust makes a charitable donation to certain donees and the donated property is a public work of art, the eligible amount of the donation can be increased by 25% or 50%, as applicable. The trust must enclose with its return a certificate, issued by the Ministère de la Culture et des Communications, confirming the fair market value (FMV) of the public work of art.

The term "public work of art" means a permanent work of art, often large in size or of an environmental nature, installed in a space accessible to the public for the purposes of commemoration, embellishment or integration into the architecture or environment of public buildings and sites.

Thus, unless the 25% increase has already been applied because the work of art is a public work of art that was donated to a Québec museum, the eligible amount of the gift can be increased by 25% if the donee was:

-

the Québec government (if the donee was an educational institution that is a mandatary of the State, refer to the following paragraph);

-

a Québec municipality or a registered municipal or public body performing a function of government in Québec (other than a school service centre governed by the Education Act) and, according to the certificate issued by the Ministère de la Culture et des Communications, the work was acquired by the municipality or body in accordance with its acquisition and conservation policy for public works of art.

The eligible amount of a donation of a public work of art can be increased by 50% if the donee was:

-

an educational institution that is a mandatary of the State;

-

a school service centre governed by the Education Act or by the Education Act for Cree, Inuit and Naskapi Native Persons;

-

a registered charity whose mission is education and that is:

-

an educational institution established under a Québec statute, other than an educational institution that is a mandatary of the State,

-

a general and vocational college (CEGEP),

-

a university-level institution referred to in one of paragraphs 1 to 11 of section 1 of the Act respecting educational institutions at the university level, or

-

an accredited private educational institution for the purposes of the grant under the Act respecting private education.

-

In this case, the certificate issued by the Ministère de la Culture et des Communications must also confirm that the work of art acquired by the donee will be installed in a place that is accessible to the students and that its conservation can be assured.

Increase in the eligible amount of a gift of an immovable intended for cultural purposes

If a trust makes a gift of a building located in Québec capable of housing artists' studios or one or more cultural organizations, the eligible amount of the gift can be increased by 25% if the three conditions below are met.

-

The gift must have been made to one of the following donees:

-

a Québec municipality or a registered municipal or public body performing a function of government in Québec;

-

a registered charity operating in Québec in the field of arts or culture;

-

a registered cultural or communications organization;

-

a registered museum.

-

-

The Ministère de la Culture et des Communications issued the trust a certificate confirming the FMV of the building (including the value of the land on which the building is located).

-

The Ministère de la Culture et des Communications issued an eligibility certificate for the building, unless the building is likely to house cultural organizations, the donation is made to one of the donees in the last three sub-bullets above and the donor has acquired the building to carry out all or part of its activities there.

Amount of charitable donations and carry-over of the unused portion

The trust is entitled to a tax credit for the total eligible amount of charitable donations. This includes donations made by the trust during the taxation year and the previous five years, as long as a tax credit has not already been granted for those donations in a previous taxation year or, if the trust is a succession, in the year of death or the previous year.

The trust may choose to claim only a portion of its total donations (to the maximum amount allowed). The unused portion can be carried forward five years.

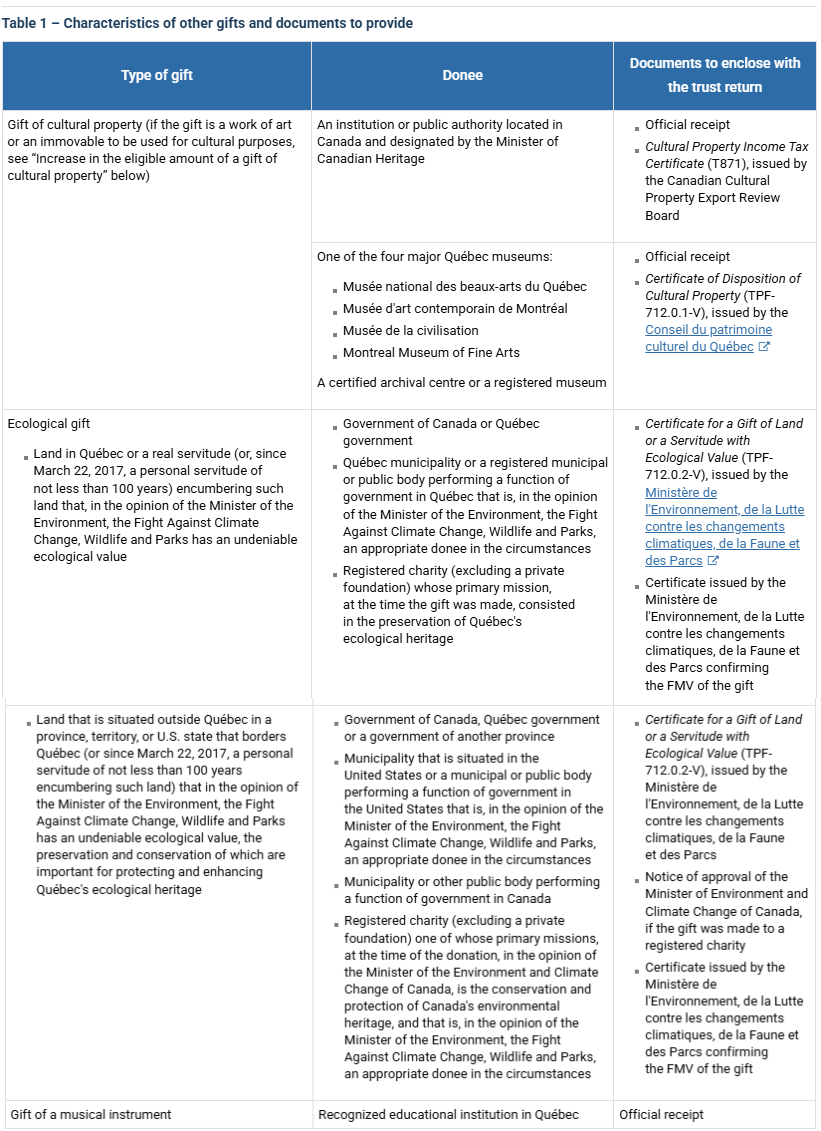

Other gifts

The table below shows the other gifts for which the trust can claim a tax credit.

Increase in the eligible amount of a gift of cultural property

The eligible amount of a gift can be increased if the cultural property is:

-

a work of art given to a museum in Québec or a recognized or accredited museum;

-

a public work of art; or

-

immovable intended for cultural purposes.

For more information, see the section on charitable donations. Note that eligible donees and the documents to enclose with the return are listed in the table above.

Gift of property with undeniable ecological value

Since March 22, 2017, the following rules have applied to gifts of property with undeniable ecological value:

-

The municipalities and municipal or public bodies performing a function of government that receive such a gift must prove to the Ministère de l'Environnement, de la Lutte contre les changements climatiques, de la Faune et des Parcs that the gifts received will be protected in the long-term.

-

Private foundations are no longer authorized to receive gifts of property with undeniable ecological value.

-

Certain gifts of personal servitudes are considered gifts of property with undeniable ecological value, provided they meet certain conditions (for example, the personal servitude must have a term of not less than 100 years).

Carry-over of the unused portion

The total eligible amount of cultural property and musical instruments can include gifts made by the trust during the taxation year and the previous five years, provided a tax credit for those gifts has not already been granted. For ecological gifts, it includes gifts made during the taxation year and in the previous ten years.

The trust can choose to claim only a portion of its total gifts. The unused portion can be carried forward five years (ten years in the case of an ecological gift). Refer to the carry-over rules for donations, which also apply to gifts of ecological property made by a GRE.

Sections 657, 657.1, 752.0.10.1, 752.0.10.2, 752.0.10.6, 752.0.10.11.1, 752.0.10.11.2, 752.0.10.15, 752.0.10.15.1, 851.33 and 999.2