Line 462 - Other credits

Line 462 - Other credits

Line 462 - Other credits

On line 462, enter the amount of the tax credit to which you are entitled and, in box 461, enter the corresponding number from the following list.

If you are claiming more than one tax credit, enter the total on line 462 and "99" in box 461.

| 01 | Refundable tax credit for medical expenses |

| 02 | Tax credit for caregivers |

| 05 | Property tax refund for forest producers |

| 06 | Tax credit for adoption expenses |

| 07 | Tax credit for an on-the-job training period |

| 08 | Tax credit for the repayment of benefits |

| 09 | Tax credit for income tax paid by an environmental trust |

| 10 | Tax credit for the reporting of tips |

| 11 | Tax credit for the treatment of infertility |

| 15 | Tax credit for scientific research and experimental development |

| 18 | Tax credit for top-level athletes |

| 19 | Tax credit for income from an income-averaging annuity for artists |

| 24 | Independent living tax credit for seniors |

| 25 | Tax credit for children's activities |

| 29 | Grant for seniors to offset a municipal tax increase |

| 30 | Tax credit for interest on a loan granted by a seller-lender and guaranteed by La Financière agricole du Québec |

| 33 | Tax credit for the upgrading of residential waste water treatment systems |

01 Refundable tax credit for medical expenses

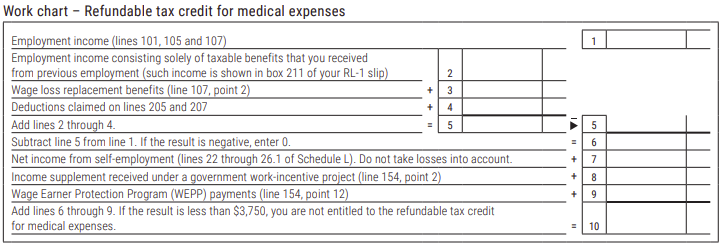

You may be entitled to the refundable tax credit for medical expenses if you meet the following conditions:

-

You were resident in Québec on December 31, 2025.

-

You were resident in Canada throughout 2025.

-

You were 18 or older on December 31, 2025.

-

Your work income is $3,750 or more (to find out whether your work income is $3,750 or more, complete the work chart below).

-

You are claiming medical expenses on line 381 or the disability supports deduction on line 250.

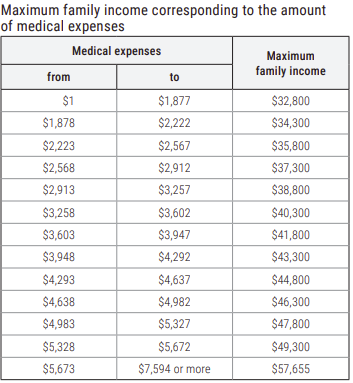

If you entered an amount on line 381, use the table opposite to find the maximum family income that corresponds to the amount of your medical expenses (line 36 of Schedule B) plus, if applicable, the disability supports deduction (line 250, point 7). Then, compare the maximum family income to your family income. Your family income is the amount on line 275 of your return plus, if you had a spouse on December 31, 2025, the amount on line 275 of your spouse's return.

If your family income is equal to or greater than the maximum family income, you are not entitled to the refundable tax credit for medical expenses. If it is less than the maximum, complete parts A and D of Schedule B.

If you did not enter an amount on line 381 but you are claiming the disability supports deduction on line 250, do not use the table opposite. Instead, complete parts A and D of Schedule B.

Your spouse was not resident in Canada throughout the year

If, for all or part of 2025, your spouse on December 31, 2025, was not resident in Canada, your family income (Part A of Schedule B) must include all of your spouse's income, including income earned while not resident in Canada.

02 Tax credit for caregivers

You may be eligible for a refundable tax credit for caregivers if you:

-

provided care to a person aged 18 or over who has a severe and prolonged impairment and needs assistance in carrying out a basic activity of daily living; or

-

provided care to and lived with a person (other than your spouse) aged 70 or over.

The maximum tax credit is $1,494 or $2,988, depending on your situation. See Schedule H for the conditions.

To claim the credit, complete Schedule H.

Advance payments of the tax credit for caregivers

If you received advance payments of the tax credit for caregivers in 2025, enter the amount from box H of your RL-19 slip on line 441.

Forms to enclose

-

Certificate Respecting an Impairment (TP-752.0.14-V)

This form is used to confirm that the care receiver has a severe and prolonged impairment in mental or physical functions and certify that they need assistance in carrying out a basic activity of daily living (Part 5). If you have already filed the certificate, do not submit it again. If the care receiver's health has improved since the last time you filed the certificate, you must inform us. -

Certificate of Ongoing Assistance (TP-1029.AN.A-V)

If the care receiver is not related to you, also enclose this form. It must be renewed every three years.

05 Property tax refund for forest producers

If, in 2025, you were a certified forest producer under the Sustainable Forest Development Act, were actively engaged in developing your woodlots and held a valid forest producer's certificate issued for that purpose, you can claim a refund for all the assessment units listed on your certificate whose total area is used for forestry purposes. To calculate the amount of your refund, complete Part C of Schedule E.

The value of the land and the total value of the unit are given on the assessment roll of a municipality, school service centre or school board.

The total property taxes on the immovable property included in the assessment units listed on your certificate is equal to the total of the following:

-

the municipal taxes paid in 2025; and

-

the school taxes paid in 2025.

To be entitled to the refund, you must have a report from a forest engineer listing your eligible development expenses (within the meaning of the Regulation respecting the reimbursement of property taxes of certified forest producers) for 2025, or you must have such expenses in reserve.

Carrying development expenses to a future year

If you incurred eligible development expenses in a given calendar year and they are greater than the property taxes you paid, you can carry them forward up to ten calendar years.

If you incurred eligible development expenses in a given calendar year before 2022 and they are less than the property taxes you paid, you can carry them forward up to five calendar years.

06 Tax credit for adoption expenses

You can claim a refundable tax credit for each child for whom you incurred eligible adoption expenses if you were resident in Québec on December 31, 2025, and any of the following conditions are met:

-

An adoption judgment establishing a bond of filiation between you and another person was rendered in 2025 by a court having jurisdiction in Québec.

-

Such a judgment rendered outside Québec received legal recognition in Québec in 2025.

-

A certificate of compliance with the Convention on Protection of Children and Co-operation in Respect of Intercountry Adoption was issued in 2025 (however, if the Minister of Health and Social Services has applied to the Court of Québec for a ruling on the validity of the certificate, you must claim the tax credit in the year in which the certificate was declared valid).

This tax credit is equal to 50% of your eligible adoption expenses. The maximum expenses are $20,000 per child, for a maximum tax credit of $10,000 per child.

Form to enclose

Tax Credit for Adoption Expenses (TP-1029.8.63-V)

07 Tax credit for an on-the-job training period

If you or a partnership of which you were a member carried on a business in Québec and paid wages to a trainee, an apprentice or a trainee/apprentice supervisor, you may be entitled to a refundable tax credit for an on-the-job training period for your qualified expenditures.

Form to enclose

Tax Credit for an On-the-Job Training Period (TP-1029.8.33.6-V)

08 Tax credit for the repayment of benefits

If, in 2025, you repaid benefits that you received in a previous year under the Québec Pension Plan (QPP), the Canada Pension Plan (CPP), the Québec parental insurance plan (QPIP) or the Employment Insurance Act, we can, at your request, calculate whether it is to your advantage to not use the repayment to reduce your 2025 income. If it is, we will grant you a tax credit for the repayment of benefits.

If you want us to do the calculation, enter the amount of the repayment on line 246 and enter "08" in box 461.

|

IMPORTANT If you chose to deduct these benefits from your income for 2019 though 2024 instead of 2025, you can ask us to determine whether it is better for you to claim the tax credit for the repayment of benefits in 2025 or the deduction for a repayment of amounts overpaid to you (line 246) for the year for which you made the choice. For more information, contact us. |

Enclose a note specifying the year to which the repayment applies. Also enclose the documents attesting to the repayment.

09 Tax credit for income tax paid by an environmental trust

You can claim this credit if you are including in your income amounts allocated by an environmental trust, that is, a trust maintained for the sole purpose of funding the reclamation of a site in Canada that is or was used mainly for one or more of the following:

-

the operation of a mine;

-

the extraction of clay, peat, sand, shale or aggregates (including dimension stone and gravel);

-

the deposit of waste; or

-

the operation of a pipeline (if the trust was created after 2011).

Form to enclose

Tax Credit for the Income Tax Paid by an Environmental Trust (CO-1029.8.36.53-V)

10 Tax credit for the reporting of tips

If you or a partnership of which you were a member carried on a business in the restaurant and hotel sector in Québec, you may be entitled to a refundable tax credit for the employer contributions that you or the partnership paid to the governments of Québec and Canada on:

-

tips received by or allocated to employees; and

-

the tip-related portion of your employees' indemnities (vacation pay and indemnities for statutory holidays, for family or parental leave and for leave taken to fulfill family obligations or for health reasons).

The credit can also apply to the employer contributions paid on an employee's tips if you control substantially all of the employee's tips because service charges are added to the bill. In such a case, the following conditions must be met:

-

The required tip is almost always at least 10% of the tippable sales.

-

Customers are informed of the compulsory tip and the percentage charged.

-

You administer any tip-sharing arrangement in effect.

Form to enclose

Tax Credit for the Reporting of Tips (TP-1029.8.33.13-V)

11 Tax credit for the treatment of infertility

You may be entitled to a refundable tax credit for expenses paid in 2025 for an in vitro fertilization or artificial insemination treatment, provided the following conditions are met:

-

You were resident in Québec on December 31, 2025.

-

The treatment is not covered by a health insurance plan.

-

The expenses were paid so that you or your spouse could have a child.

To find out what expenses are eligible and calculate the amount of the credit you can claim, complete form TP-1029.8.66.2-V, Tax Credit for the Treatment of Infertility. Enclose the form with your return.

Advance payments of the tax credit for the treatment of infertility

If you received advance payments of the tax credit for the treatment of infertility in 2025, enter the amount from box G of your RL-19 slip on line 441 of your return.

15 Tax credit for scientific research and experimental development

You may be entitled to a refundable tax credit if you operated a business in Canada, you carried out scientific research and experimental development (R&D) or had R&D carried out on your behalf, and your taxation year began before March 26, 2025.

Likewise, you may be eligible for a refundable tax credit if you are a member of a partnership that operated a business in Canada and carried out R&D or had R&D carried out on its behalf, and whose fiscal period began before March 26, 2025.

|

IMPORTANT This tax credit has been eliminated for taxation years and fiscal periods beginning after March 25, 2025. It has been replaced by the new tax credit for R&D and pre-commercialization, which can only be claimed by corporations and corporations that are members of a partnership. |

Forms to enclose

-

Tax Credit for Salaries and Wages (R&D) (RD-1029.7-V)

-

Tax Credit for University Research or Research Carried Out by a Public Research Centre or a Research Consortium (RD-1029.8.6-V)

-

Tax Credit for Fees and Dues Paid to a Research Consortium (RD-1029.8.9.03-V)

-

Tax Credit for Private Partnership Pre-Competitive Research (RD-1029.8.16.1-V)

18 Tax credit for top-level athletes

If you were resident in Québec on December 31, 2025, and, for 2025, were recognized as a top-level athlete by the Ministère de l'Éducation, you may be entitled to a refundable tax credit. Only athletes can claim this credit.

To claim the credit, enter on line 462 the amount shown on the certificate issued to you by the Ministère. Keep the certificate on file in case we ask for it.

19 Tax credit for income from an income-averaging annuity for artists

If you were resident in Québec on December 31, 2025 (or on the day you ceased to be resident in Canada in 2025), you included in your income amounts from an income-averaging annuity for artists and income tax was withheld from the annuity, you may be entitled to a refundable tax credit.

Enter the amount shown in box C-9 of your RL-2 slip.

24 Independent living tax credit for seniors

You may be entitled to this refundable tax credit for expenses you incurred as a senior in order to continue living independently if you meet both of the following conditions:

-

You were resident in Québec on December 31, 2025.

-

You were 70 or older on December 31, 2025.

This tax credit is equal to 20% of the total of the following expenses:

-

expenses incurred for the purchase, lease or installation of eligible equipment or fixtures (the first $250 of such expenses is not eligible for the tax credit);

-

expenses incurred for one or more stays in a functional rehabilitation transition unit.

The expenses must have been paid by you or your spouse.

To claim the tax credit, complete Part E of Schedule B.

Expenses for the purchase, lease and installation of eligible equipment or fixtures

The expenses must have been paid in 2025 to purchase, lease or install any of the following equipment or fixtures intended for use in your principal residence:

-

a person-centred remote monitoring device, such as an emergency call device ("panic button"), a device for remotely measuring various physiological parameters or a device for remotely supervising the taking of medication;

-

a personal GPS locator;

-

a device designed to assist a person in getting on or off a toilet;

-

a device designed to assist a person in getting into or out of a bathtub or shower;

-

a walk-in bathtub or shower;

-

a mechanized, rail-mounted chair lift designed to carry a person up or down a stairway;

-

a hospital bed;

-

an alert system for individuals with hearing impairments (for example, a vibrotactile aid, a telephone monitor, a door monitor, a fire alarm monitor, a sound monitor or an adapted alarm clock [visual, tactile or for deaf-blind persons]);

-

hearing aids;

-

a rollator or walker;

-

a cane or crutches;

-

a non-motorized wheelchair.

Expenses incurred for one or more stays in a functional rehabilitation transition unit

The expenses must have been paid in 2025 for your stay or stays in a functional rehabilitation transition unit that began in 2025 or in 2024.

You can claim the expenses incurred for the first 60 days of any given stay as follows:

-

If your stay lasted 60 days or less, you can claim all of the expenses incurred for the stay.

-

If your stay lasted more than 60 days, you can claim only the expenses incurred for the first 60 days.

There is no limit to the number of stays. For example, if you incurred expenses for two stays in a functional rehabilitation transition unit in 2025, and your first stay lasted 35 days and your second stay lasted 70 days, you can claim:

-

all the expenses incurred for the 35-day stay; and

-

the expenses incurred for the first 60 days of the 70-day stay.

Functional rehabilitation transition unit

A public or private resource offering accommodation and services focusing on re-education and rehabilitation for seniors who are experiencing a loss of autonomy but who will be able to return home after hospitalization.

Expenses that were reimbursed or used to calculate another tax credit

You cannot claim the independent living tax credit for seniors for any of the following expenses:

-

expenses for which you, your spouse or someone else received or is entitled to receive a reimbursement, unless the reimbursement was included in that person's income and cannot be deducted elsewhere in that person's income tax return (such as on line 236 or 297);

-

expenses included in the calculation of another refundable or non-refundable tax credit claimed by you, your spouse or someone else, such as a tax credit for medical expenses or the tax credit for home-support services for seniors.

25 Tax credit for children's activities

You can claim a refundable tax credit for the physical activities or artistic, cultural or recreational activities of an eligible child, provided you meet all of the following conditions:

-

You were resident in Québec on December 31, 2025.

-

In 2025, you or your spouse on December 31, 2025 (see the definition at line 12), paid to either:

-

register the child in a program that is not part of a school's curriculum and that includes physical activities or artistic, cultural or recreational activities for children that take place over at least eight consecutive weeks or at least five consecutive days (in the case of a summer camp, for example); or

-

obtain a membership for the child in a club, association or similar organization that offers physical activities or artistic, cultural or recreational activities for children, provided that the membership is for a minimum period of eight consecutive weeks.

-

-

Your family income does not exceed $168,470 (your family income is the amount on line 275 of your return plus, if applicable, the amount on line 275 of the return of your spouse on December 31, 2025).

-

You have a receipt that constitutes proof of payment of eligible registration or membership fees. You must keep your receipt in case we ask for it.

|

NOTE

|

You or your spouse was not resident in Canada throughout the year

If, for all or part of 2025, you or your spouse was not resident in Canada, you must take into account, in calculating your family income, all the income you and your spouse earned, including any income earned while you or your spouse was not resident in Canada.

Physical activity

-

Any activity that contributes to cardiorespiratory endurance and the development of muscular strength, muscular endurance, flexibility or balance.

-

Any activity that enables a child with a severe and prolonged impairment in mental or physical functions to move around and expend energy in a recreational context.

|

NOTE Physical activities include horseback riding but not activities where a child rides on or in a motor vehicle. |

Artistic, cultural or recreational activity

Any activity that:

-

is intended to contribute to the child's ability to develop creative skills or expertise, acquire and apply knowledge, or improve dexterity or coordination in an artistic, cultural or recreational discipline, such as:

-

literary arts (for example, poetry, novels, storytelling, narrative literature, fictional essays and short stories),

-

visual arts (for example, photography, painting, drawing, design, sculpture and architecture),

-

performing arts (for example, theatre, dance, singing, circus acts and miming),

-

music,

-

media (for example, radio, television, film, video and digital arts),

-

languages, customs and heritage;

-

-

provides a substantial focus on wilderness and the natural environment;

-

assists with the development and use of intellectual skills;

-

includes structured interaction among children where supervisors teach or assist children to develop interpersonal skills;

-

provides enrichment or tutoring in academic subjects.

Eligible child

A child who was born:

-

after December 31, 2008, but before January 1, 2020; or

-

after December 31, 2006, but before January 1, 2020, if the child has a severe and prolonged impairment in mental or physical functions (see the instructions for line 376).

|

NOTE An eligible child can be:

|

Calculating the tax credit

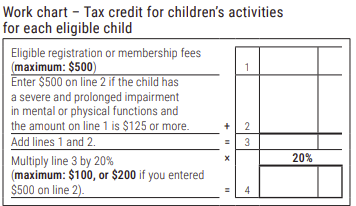

The tax credit is equal to 20% of the eligible registration or membership fees. You can claim a maximum of $500 in fees per child, for a maximum tax credit of $100 per child. If the child has a severe and prolonged impairment in mental or physical functions and the eligible fees are $125 or more, you can add $500 to the amount of the fees. However, the total ($500 plus the amount of the eligible fees) cannot exceed $1,000 per child, for a maximum tax credit of $200 per child.

Use the work chart opposite to calculate the amount of the tax credit to which you are entitled. Calculate a separate amount for each eligible child and then add up the amounts for all the eligible children. Carry the total to line 462 of your income tax return.

Splitting the tax credit

If another person is also entitled to this tax credit for the same eligible child, you can split the credit. While you can choose how you split it, the total amount claimed by both of you cannot exceed the amount to which you would have been entitled if only one of you were claiming the credit.

Fees that are not eligible

You cannot claim the tax credit for any of the following:

-

fees paid for a program of activities offered by a person who, at the time of payment, was either your spouse or under 18 years of age;

-

fees for which anyone (you, your spouse or another person) received, or is entitled to receive, a reimbursement, unless the reimbursement was included in that person's income and the reimbursement cannot be deducted elsewhere in that person's income tax return;

-

fees that were used to calculate another deduction or refundable or non-refundable tax credit claimed by you, your spouse or another person;

-

fees paid for a sports-study (Sport-Études) program or an arts-study (Art-Études) program.

29 Grant for seniors to offset a municipal tax increase

You may be entitled to a grant to help offset an increase in the municipal taxes payable on your residence if you meet the following conditions:

-

On December 31, 2025, you:

-

were resident in Québec;

-

were 65 or over; and

-

had owned your residence for at least 15 consecutive years (including any time your spouse owned the residence before you became the owner).

-

-

Your residence is an entirely residential assessment unit consisting of only one dwelling and it serves as your principal residence.

-

You received (or were entitled to receive) a municipal tax bill in your name for the residence for 2026. (If you co-owned the residence, the bill may have been issued in another co-owner's name.)

-

Your family income for 2025 does not exceed the eligibility cap.

You must also meet at least one of the following two conditions:

-

The potential grant (determined using the current assessment roll) is shown on either your 2026 municipal tax bill or the document entitled Amount of the Potential Grant to Offset a Municipal Tax Increase that was issued by your municipality.

-

You or a co-owner of the residence received a grant in the last year covered by the previous assessment roll.

For the complete list of conditions, including the maximum eligible family income, or to calculate the amount of the grant, complete form TP-1029.TM-V, Grant for Seniors to Offset a Municipal Tax Increase. Enclose the form with your return.

30 Tax credit for interest on a loan granted by a seller-lender and guaranteed by La Financière agricole du Québec

You may be entitled to a refundable tax credit if you (or a partnership of which you are a member) paid interest on a loan granted by a seller-lender after December 2, 2014, but before January 1, 2025, and guaranteed by La Financière agricole du Québec.

The credit is equal to either 40% of the interest attributable to 2025 that you paid or 40% of your share of such interest paid by the partnership of which you are a member.

Form to enclose

Tax Credit for Interest on a Loan Granted by a Seller-Lender and Guaranteed by La Financière agricole du Québec (TP-1029.8.36.VP-V)

33 Tax credit for the upgrading of residential waste water treatment systems

You may be entitled to this tax credit if all of the following conditions are met:

-

You were resident in Québec on December 31, 2025 (or on the day you ceased to reside in Canada in 2025).

-

You or your spouse had work done to upgrade the residential waste water treatment system of an eligible dwelling under a contract entered into with a qualified contractor after March 31, 2017, but before April 1, 2027 (generally speaking, an eligible dwelling is a dwelling you own in Québec that is your principal residence or, subject to certain conditions, a cottage).

-

The expenditures incurred for the work were paid in 2025.

Form to enclose

Tax Credit for the Upgrading of Residential Waste Water Treatment Systems (TP-1029.AE-V)